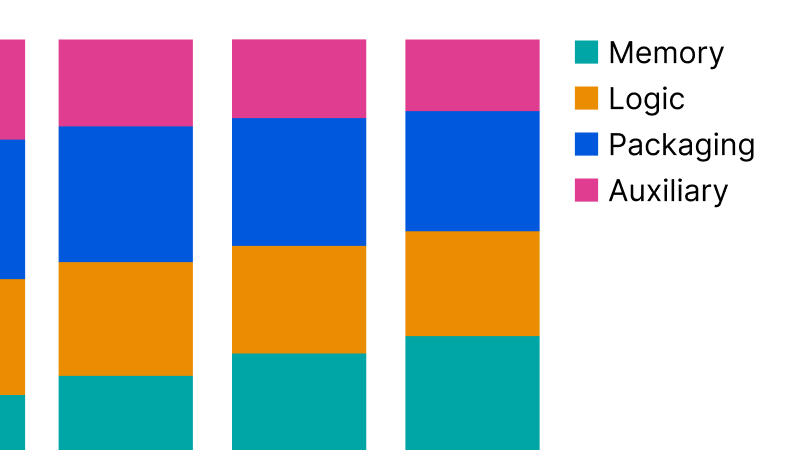

High-bandwidth memory (HBM) has become the dominant cost in AI chip manufacturing, rising from 52% to 63% of total component spending between the first quarter of 2024 and the fourth quarter of 2025, according to a new analysis from Epoch AI.

The estimates, compiled by researcher Venkat Somala, cover AI chips designed by Nvidia, AMD, Google, and Amazon, weighted by production volume. The analysis breaks down component spending into four categories: HBM memory, logic dies, advanced packaging (CoWoS), and auxiliary components.

Memory's growing share

Logic dies maintained a roughly flat share near 13% over the period. Meanwhile, advanced packaging fell from 19% to 15% of total spending, and auxiliary components dropped from 15% to 9%.

In absolute terms, the shift is even more pronounced. Total component spending on AI chips grew from approximately $22 billion in 2024 to $52 billion in 2025. HBM spending alone accounted for roughly $20 billion of that increase, jumping from about $12 billion to $32 billion over the same period. That year-over-year growth was faster than any other component category.

Hyperscaler capex reflects higher prices

The trend is expected to continue in 2026 as memory supply remains tight and prices keep rising. Major cloud providers have already begun factoring higher component costs into their capital expenditure plans.

Microsoft's $190 billion fiscal year 2026 capex outlook includes approximately $25 billion attributed to higher component prices. Meta also raised its 2026 capex range by $10 billion, citing higher component prices as a key factor.

Stay updated

Get the day's AI and automation news in your inbox. No spam, unsubscribe anytime.

Methodology and data sources

Epoch AI's analysis draws on its AI Chip Components explorer, which builds chip-level bills of materials from financial disclosures, supplier filings, and analyst reports. For each chip designed by Nvidia, AMD, Google, and Amazon, the researchers estimated per-chip costs for each of the four component categories. They then multiplied those costs by estimated quarterly production volumes to arrive at total component spending per quarter from Q1 2024 through Q4 2025.

The component categories tracked are HBM, logic dies, advanced packaging (CoWoS), and auxiliary components. The methodology documentation for the explorer provides additional detail on how each category is estimated.

Uncertainty in estimates

Each component unit carries some cost uncertainty, including the price of an HBM stack, a logic die, or a CoWoS package. Epoch AI models each chip's per-component cost with a 90% confidence interval. Because the component share is a ratio of that component's cost over total cost, both the numerator and denominator carry uncertainty.

The analysis shows two bounds on the share to account for this variability. Component costs can vary by contract, supplier, and timing, and estimates of quarterly production volumes and chip-type mix also introduce uncertainty that propagates into the reported shares.

Despite these caveats, the trend is clear: memory has become the largest and fastest-growing cost in AI chip production, and this shift is reshaping how hyperscalers budget for AI infrastructure.